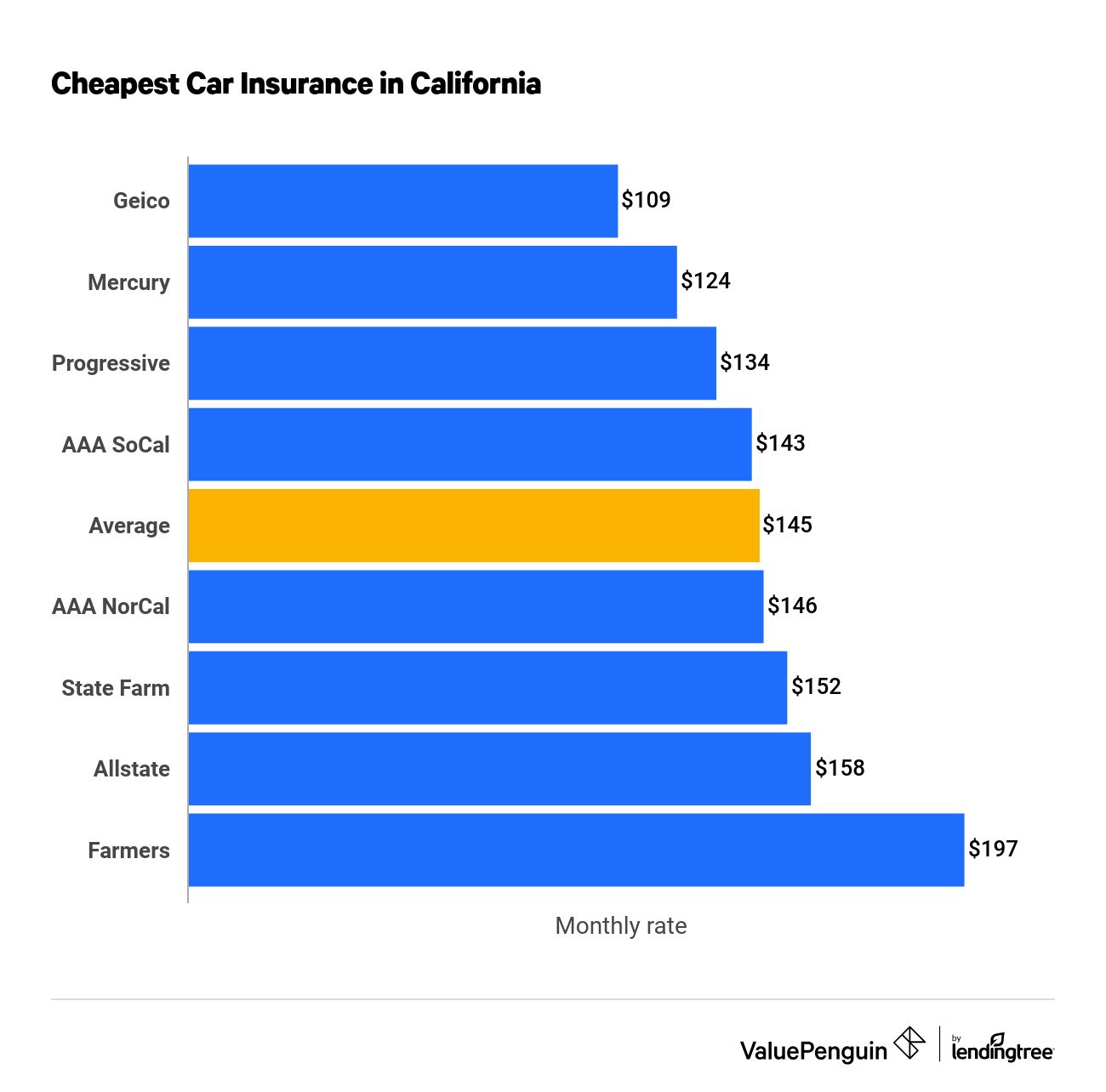

Best Car Insurance for Families Finding the Right Coverage

Best car insurance for families is more than just a policy; it’s a crucial investment in your loved ones’ safety and financial security. Choosing the right coverage involves understanding various factors, from the number of drivers and vehicle types to your location and desired level of protection. This guide navigates the complexities of family car insurance, empowering you to make informed decisions and secure the best possible protection for your family.

We will explore the key elements influencing your insurance costs, including driver demographics, vehicle details, and coverage options. We’ll also delve into the different types of policies available, helping you compare bundled versus individual plans and understand the advantages and disadvantages of each. Finally, we’ll equip you with practical strategies for finding the best deals, negotiating premiums, and understanding your policy documents.

Factors Influencing Family Car Insurance Costs

Several factors significantly impact the cost of car insurance for families. Understanding these factors allows for better budget planning and informed decision-making when choosing a policy.

Number of Drivers

The more drivers in a household, the higher the insurance premium tends to be. This is because each driver presents a separate risk profile to the insurance company. A household with multiple young, inexperienced drivers will typically pay more than a household with experienced, older drivers.

Driver Age and Driving History, Best car insurance for families

Younger drivers, especially those with limited driving experience, are statistically more likely to be involved in accidents. Therefore, their insurance premiums are generally higher. A clean driving record with no accidents or traffic violations significantly reduces insurance costs, while past incidents can lead to increased premiums.

Vehicle Type and Value

The type and value of the vehicle directly influence insurance costs. Sports cars and luxury vehicles are generally more expensive to insure due to their higher repair costs and greater risk of theft. Older, less valuable cars typically have lower insurance premiums.

Location

Geographic location plays a crucial role in determining insurance rates. Areas with higher crime rates, more accidents, or higher repair costs tend to have higher insurance premiums. Urban areas often have higher rates than rural areas.

Coverage Levels

The level of coverage chosen significantly impacts the cost of insurance. Higher coverage limits (liability, collision, comprehensive) result in higher premiums but offer greater financial protection in case of an accident or damage.

Coverage Cost Comparison

| Coverage Level | Liability | Collision | Comprehensive | Total Estimated Annual Premium |

|---|---|---|---|---|

| Minimum State Requirements | $25,000/$50,000/$10,000 | N/A | N/A | $500 |

| Standard Coverage | $100,000/$300,000/$50,000 | $500 deductible | $500 deductible | $1200 |

| Comprehensive Coverage | $250,000/$500,000/$100,000 | $250 deductible | $250 deductible | $1800 |

| Premium Coverage | $500,000/$1,000,000/$250,000 | $100 deductible | $100 deductible | $2500 |

Note: These are estimated premiums and will vary based on individual circumstances.

Types of Family Car Insurance Policies

Families have several options when choosing a car insurance policy. Understanding the differences between bundled and individual policies is crucial for selecting the best fit.

Bundled vs. Individual Policies

Source: cloudinary.com

Bundled policies combine multiple types of insurance, such as auto, home, and renters insurance, often resulting in discounts. Individual policies cover only one type of insurance. For families, bundled policies can offer significant cost savings.

Benefits and Drawbacks

- Bundled Policies: Benefits include cost savings and convenience. Drawbacks might include less flexibility in choosing individual coverage options.

- Individual Policies: Benefits include greater flexibility in choosing coverage levels for each type of insurance. Drawbacks might include higher overall costs compared to bundled options.

Common Coverage Options

Common coverage options include liability, collision, comprehensive, uninsured/underinsured motorist, and medical payments coverage. Liability coverage protects against financial responsibility for accidents you cause. Collision and comprehensive cover damage to your vehicle. Uninsured/underinsured motorist protects you if involved in an accident with an uninsured driver. Medical payments coverage helps pay for medical expenses regardless of fault.

Optional Add-ons

Optional add-ons such as roadside assistance, rental car reimbursement, and gap insurance can provide additional protection and convenience.

Policy Type Comparison

- Bundled: Often cheaper, convenient, but less flexible.

- Individual: More flexible, potentially more expensive, requires managing multiple policies.

Finding the Best Family Car Insurance Deal: Best Car Insurance For Families

Securing the best car insurance deal involves careful comparison and strategic planning. This section Artikels key steps and strategies.

Key Features to Consider

When comparing providers, consider factors like coverage options, customer service, claims process, discounts, and overall price. Read online reviews and check company ratings.

Obtaining Quotes

Obtain quotes from multiple insurance companies using online comparison tools or contacting providers directly. Provide accurate information to ensure accurate quotes.

Negotiating Lower Premiums

Negotiate with insurance providers by highlighting your good driving record, safety features in your vehicle, and willingness to bundle policies. Consider increasing your deductible to lower premiums.

Avoiding Common Pitfalls

Avoid common mistakes like failing to compare quotes, accepting the first offer, and not understanding your policy’s details.

Step-by-Step Guide

- Gather information about your vehicles and drivers.

- Use online comparison tools to get quotes.

- Contact insurers directly to discuss coverage options and negotiate.

- Carefully review policy documents before purchasing.

- Regularly review your policy to ensure it meets your needs.

Understanding Insurance Policy Documents

Thoroughly understanding your car insurance policy is crucial. This section details key aspects of policy documents.

Key Sections and Terms

Common sections include declarations page (personal information and coverage details), insuring agreement (what is covered), exclusions (what is not covered), conditions (policy rules), and definitions (key terms).

Coverage Limits and Deductibles

Coverage limits represent the maximum amount the insurer will pay for a claim, while the deductible is the amount you pay out-of-pocket before the insurer covers the rest.

Exclusions and Limitations

Policies typically exclude coverage for intentional acts, damage caused by wear and tear, and certain types of accidents.

Filing a Claim

In case of an accident, promptly report the incident to your insurer, gather necessary information (police report, witness statements), and follow the insurer’s claim process.

Sample Policy Summary

A typical policy summary might include the policy number, insured’s name, coverage details (liability limits, collision and comprehensive coverage, deductibles), premium amount, and effective dates. It will also usually include contact information for claims and customer service.

Safety Features and Discounts

Vehicle safety features and responsible driving habits can significantly influence insurance premiums. Many insurers offer discounts for demonstrating safe driving practices and equipping vehicles with safety technology.

Impact of Safety Features

Vehicles equipped with advanced safety features such as anti-lock brakes (ABS), electronic stability control (ESC), airbags, and advanced driver-assistance systems (ADAS) often qualify for lower insurance premiums due to their accident-reducing capabilities.

Discounts for Families

Many insurers offer discounts for families, including multi-car discounts (for insuring multiple vehicles under one policy), good driver discounts (for maintaining a clean driving record), and safe-driver programs (for participating in telematics programs that monitor driving behavior).

Examples of Qualifying Safety Features

Source: com.ph

- Anti-lock brakes (ABS)

- Electronic stability control (ESC)

- Airbags (front, side, curtain)

- Backup cameras

- Forward collision warning systems

- Lane departure warning systems

- Adaptive cruise control

- Automatic emergency braking

Discount Comparison

Discount amounts vary significantly among insurance providers. Some may offer a percentage discount, while others may offer a fixed dollar amount reduction in premiums. It’s essential to compare offers from multiple insurers to find the best deal.

Visual Representation of Safety Feature Impact

Imagine a graph with safety features on the x-axis and insurance cost on the y-axis. As the number and sophistication of safety features increase (e.g., from basic ABS to a full suite of ADAS), the insurance cost gradually decreases, showing a negative correlation between safety features and premium cost. The slope of the decrease would vary depending on the insurer and specific safety features.

Summary

Securing the best car insurance for your family requires careful consideration of numerous factors, but with the right knowledge and approach, the process becomes manageable and even rewarding. By understanding the influence of driver profiles, vehicle characteristics, location, and coverage levels, you can effectively compare policies and negotiate favorable terms. Remember to prioritize comprehensive coverage that aligns with your family’s needs and budget, and always review your policy documents thoroughly.

Empowered with this information, you can confidently protect your family and your finances on the road.

User Queries

What is the difference between liability and collision coverage?

Liability coverage pays for damages or injuries you cause to others in an accident. Collision coverage pays for repairs to your vehicle regardless of fault.

How often can I expect my insurance premiums to change?

Premiums can change annually, or even more frequently depending on your insurer and any changes in your driving record or policy.

Can I get a discount for having multiple cars insured with the same company?

Yes, many insurers offer multi-car discounts to incentivize bundling your policies.

What should I do if I need to file a claim?

Contact your insurance company immediately after an accident to report the incident and follow their claim filing procedures.