Affordable Renters Insurance for Studio Apartments USA

Affordable renters insurance for studio apartments USA is a crucial yet often overlooked aspect of securing your living space. Finding the right balance between comprehensive coverage and affordable premiums can feel daunting, but understanding the key factors involved empowers renters to make informed decisions. This guide navigates the complexities of renters insurance, providing insights into coverage options, cost considerations, and reputable providers to help you find the perfect fit for your studio apartment.

This exploration delves into defining “affordable” within the context of renters insurance for studio apartments across various US regions, considering factors such as location, coverage level, and deductible choices. We’ll examine essential coverage components—personal property, liability, and additional living expenses—and illustrate their relevance through real-life scenarios. The guide also provides a comparative analysis of leading renters insurance providers, highlighting their pricing structures, features, and customer reviews to assist in your selection process.

Furthermore, we’ll discuss strategies for securing lower premiums without sacrificing essential protection and address common policy exclusions and limitations.

Defining “Affordable” Renters Insurance: Affordable Renters Insurance For Studio Apartments USA

The definition of “affordable” renters insurance varies significantly depending on individual financial situations and geographical location. While there’s no single nationwide standard, a reasonable range for studio apartment renters insurance in the USA could be considered between $10 and $30 per month. However, this can fluctuate substantially. Factors influencing the cost are discussed below.

Factors Influencing Renters Insurance Cost

Several factors play a crucial role in determining the price of renters insurance. Location is a primary driver; renters in high-crime areas or regions prone to natural disasters will typically pay more. The level of coverage selected directly impacts cost; higher coverage limits naturally lead to higher premiums. Finally, the deductible chosen – the amount you pay out-of-pocket before insurance coverage kicks in – also affects the premium; higher deductibles usually mean lower premiums.

Coverage Features at Different Price Points

Lower-priced policies often offer basic coverage for personal property and liability, with lower coverage limits. Mid-range policies typically include broader coverage amounts and might add features like additional living expenses (ALE) coverage. Higher-priced policies may offer more comprehensive coverage, higher limits, and additional endorsements, such as coverage for valuable items or specific perils.

Coverage Options for Studio Apartments

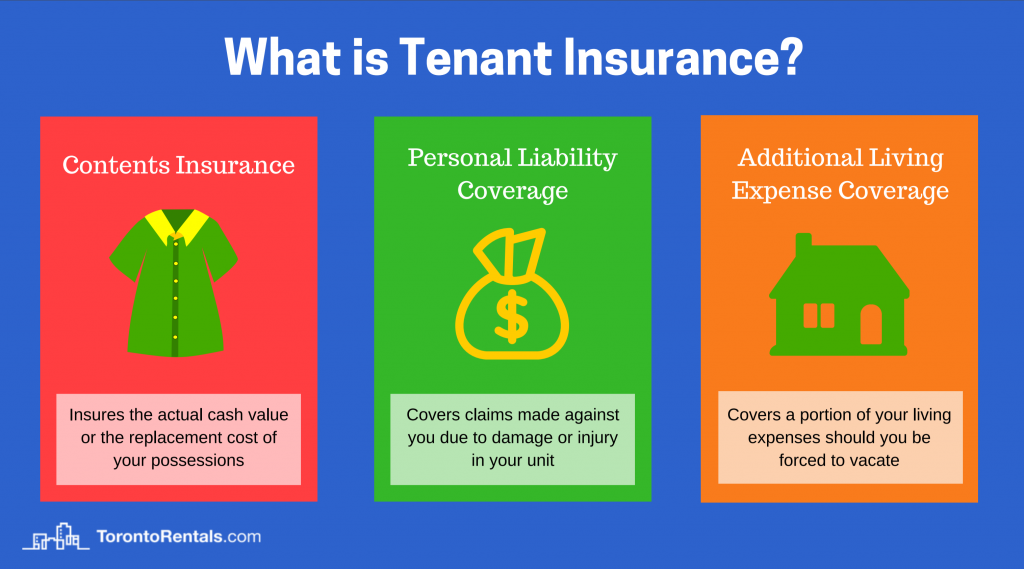

Renters insurance for a studio apartment, while seemingly simple, requires careful consideration of essential coverage components to ensure adequate protection.

Essential Coverage Components

Three key components are crucial for studio apartment renters: personal property coverage protects your belongings from damage or theft; liability coverage protects you financially if you accidentally injure someone or damage their property; and additional living expenses (ALE) coverage helps cover temporary housing and living costs if your apartment becomes uninhabitable due to a covered event.

Examples of Beneficial Coverage Scenarios

- Personal Property: A burst pipe damages your laptop and furniture. Personal property coverage would help replace or repair them.

- Liability: A guest trips and falls in your apartment, injuring themselves. Liability coverage would help pay for their medical bills and any legal costs.

- Additional Living Expenses (ALE): A fire renders your apartment unlivable. ALE coverage would help pay for temporary lodging, meals, and other essential expenses while repairs are underway.

Sample Renters Insurance Policy for a Studio Apartment

Source: torontorentals.com

A sample policy might include coverage for personal property up to $10,000, liability coverage of $100,000, and ALE coverage of $5,000. Exclusions would typically include damage caused by floods, earthquakes (unless specifically added), and intentional acts.

Finding Affordable Renters Insurance Providers

Several major renters insurance providers offer nationwide coverage in the USA. Comparing their offerings is essential to find the best value.

Comparison of Renters Insurance Providers

| Provider | Price Range (Monthly) | Key Features | Customer Reviews Summary |

|---|---|---|---|

| Lemonade | $5 – $25 | AI-powered claims, easy online process | Generally positive, praised for speed and ease of use |

| State Farm | $10 – $35 | Wide range of coverage options, established reputation | Mixed reviews, some complaints about claims processing |

| Allstate | $12 – $40 | Bundling discounts, various coverage levels | Mixed reviews, similar to State Farm |

| USAA | $8 – $28 | Excellent customer service (military members and families) | Highly positive reviews, known for strong customer support |

| Progressive | $10 – $30 | Name your price tool, online management | Mostly positive, praised for ease of use and online tools |

Online Marketplaces vs. Individual Providers

Online marketplaces offer convenient comparison shopping, but may lack the personalized service of contacting individual providers directly. Individual providers may offer more tailored policies and potentially better rates for long-term customers, but require more legwork in comparing options.

Factors Affecting Insurance Premiums

Several factors influence the cost of your renters insurance premiums. Understanding these factors can help you secure more affordable coverage.

Impact of Credit Score, Claims History, and Location

A good credit score can often lead to lower premiums. A history of claims may increase premiums. Location, as mentioned, significantly affects cost due to varying risk levels.

Improving Chances of Lower Premiums

Source: turbotenant.com

Maintaining a good credit score, avoiding claims by taking preventative measures (e.g., installing smoke detectors), and bundling insurance policies can all help lower premiums. Choosing a higher deductible can also reduce your monthly payments.

Tips for Lowering Renters Insurance Costs

- Shop around and compare quotes from multiple providers.

- Increase your deductible.

- Bundle your renters insurance with other policies (auto, etc.).

- Maintain a good credit score.

- Consider a higher deductible to lower premiums.

Understanding Policy Exclusions and Limitations

It’s crucial to understand what your renters insurance policy doesn’t cover to avoid unexpected costs.

Common Exclusions, Affordable renters insurance for studio apartments USA

Common exclusions include damage caused by floods, earthquakes, war, and intentional acts. Specific items, such as cash and valuable jewelry, may require separate endorsements for higher coverage limits.

Examples of Uncovered Events or Items

- Damage caused by a flood.

- Loss of cash or valuable jewelry exceeding policy limits.

- Damage resulting from a nuclear accident.

Questions to Ask Your Insurance Provider

- What are the specific exclusions in my policy?

- What is the coverage limit for my personal property?

- What is the process for filing a claim?

- What are the deductibles for different types of claims?

Illustrative Scenarios and their Coverage

Understanding how renters insurance responds to various scenarios is essential. Here are a few examples.

Theft of Personal Belongings

Imagine a scenario where your studio apartment is burglarized, and your laptop, television, and other electronics are stolen. Your personal property coverage would help replace these items, up to your policy’s coverage limit, minus your deductible.

Liability Coverage Scenario

Suppose you accidentally spill a glass of red wine on your neighbor’s expensive rug while visiting their apartment. Your liability coverage would help pay for the cost of cleaning or replacing the damaged rug, preventing a costly dispute.

Additional Living Expenses (ALE) Coverage After a Fire

Smoke fills the air, the smell of burnt wood hangs heavy, and your studio apartment is severely damaged by a fire. Your apartment is uninhabitable. ALE coverage would provide funds for temporary housing (hotel, Airbnb), meals, and other necessary living expenses until your apartment is repaired or rebuilt. This could cover rent for a temporary apartment, costs associated with finding alternative housing, and essential daily living expenses while you are displaced.

Final Thoughts

Securing affordable renters insurance for your studio apartment in the USA doesn’t have to be a complex undertaking. By carefully considering your needs, comparing provider options, and understanding the factors influencing premiums, you can confidently choose a policy that provides adequate protection without breaking the bank. Remember to thoroughly review policy details, ask clarifying questions, and leverage resources like online comparison tools to find the best fit for your budget and lifestyle.

Protecting your belongings and mitigating potential liabilities is a worthwhile investment, ensuring peace of mind in your studio apartment.

User Queries

What is the average cost of renters insurance for a studio apartment in the US?

The average cost varies greatly by location, coverage, and deductible. Expect to pay anywhere from $10 to $30 per month, but it’s crucial to obtain quotes from multiple providers.

Can I get renters insurance if I have a poor credit score?

Yes, but a poor credit score may lead to higher premiums. Some insurers place less emphasis on credit than others, so it’s worth comparing quotes across different providers.

What if I only have a few valuable possessions? Do I still need renters insurance?

Yes, even if you have few possessions, liability coverage is crucial. Renters insurance protects you against lawsuits if someone is injured in your apartment, regardless of the value of your belongings.

How long does it take to get a renters insurance policy?

Notice best auto insurance for high-value cars in the USA for recommendations and other broad suggestions.

Many online providers offer instant quotes and policy issuance. Traditional providers may take a few days to process your application.